On 2/23/11, Interface Inc. (IFSIA) reported a decent 4Q’10, meeting analysts’ consensus expectations of $0.21 (actually beating them ever slightly). Press Release

Overall, we have few issues with the company, so will report only key points…

- Backlog was good (+15% Y/Y) but less than the previous quarter (+20% y/y). This was due to inclement weather, as we’re all too familiar w/ this winter.

- The company’s customer diversification strategy is tracking well. For example, sales outside of traditional offices (such as retailers, education) picked up during the quarter.

- Raw material costs rose about 5%, and the company is likely to raise prices. However, given the still-weak US Consumer Economy, we don’t expect the company will be able to continue such a strategy in 2011/12 unless economic growth accelerates. Also, raw prices are likely to remain high, given Mideast Turmoil and high demand for most commodities in Emerging Markets.

- The Chinese plant opened, but is still not profitable (as expected). We still think this is the key plant and market to watch. So far, both are tracking well. While small, Emerging Markets are continuing to grow quickly and show that Interface made a wise decision to invest in a new Chinese plant.

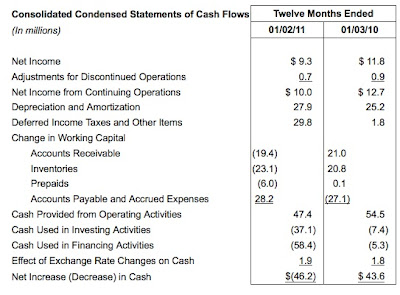

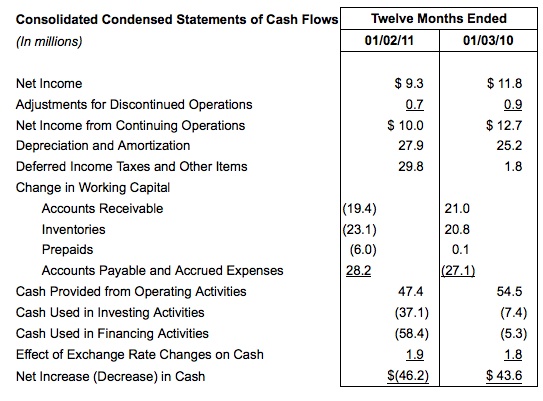

- However, these new investments are keeping Free Cash Flow at bay. FCF was just $10MM for full year 2010. As a result, FCF for 2011 may be a bit lower than I had predicted in my original Analysis (the above is due to simultaneous increase in Capex and lower operating cash flow than expected).

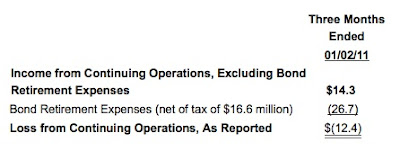

Note that the company reported Non-GAAP numbers, but we are of the belief that such numbers are valid given that the company had a one-time Bond Refinancing that is truly a non-recurring event.

Conclusion: A good quarter for IFSIA, would have been even better, if well, Mother Nature was in a better mood. Looking forward to continued momentum on existing trends.