EVERY DAY ONE HEARS THE UNENDING MARCH OF THE CHINESE ECONOMY. China is large, powerful and growing quickly.

France is the world’s 4th largest economy, and its influence is even larger; as it has the second largest number of diplomatic missions in the world. Its Revolution inspired motto is: Liberté, Égalité, Fraternité. In plain English, the “jist” of this motto is having one’s citizen’s treated fairly, with freedoms as we have in the States, and that one looks out for the common good. Ah, could this be the roots of modern SRI?

France is the 14th ranked on the Human_Development_Index. Countries in this index tend to also have the most advanced SRI initiatives. The Netherlands is ranked even higher (number 7). It also happens to manage one of the highest levels of SRI assets in Europe, at EUR 130 billion.

Size & Growth of French SRI:

French involvement in Socially Responsible Investing is large, at EUR 50.7bn, and growing quickly. SRI assets grew 70% in 2009 (latest available data) on top of 37% growth in 2008. The 2008 growth, while smaller is spectacular considering it occurred in the midst of the global Financial Crises. This data is sourced from Novethic.com (which is part of the French pension system). While 2010 data is yet to be published, we expect another double-digit growth number given recent trends.

|

| Source: Novethic SRI Research Center |

By Asset Type:

Drilling down, the largest growth came from Mutual Funds, which Novethic labels Collective Management. Within Mutual Funds, the largest growth area was to Retail investors. Employee Savings was also a very large contributor. This includes 401K type plans. Note that while the Retail Investor grew rapidly, Institutional Investors still dominate the French SRI market (69% vs 31% for retail investors).

Employee Savings examined:

SRI employee savings benefited from the conversion of bond and money market funds, with those assets nearly doubling. The proportion, or share, of employee savings funds in SRI rose from 8% to 13%. As US readers probably already noticed, few United States savings plans offer such options.

Given that capital markets were so strong in 2009, one wonders whether the sharp growth was due to strong markets. Well, Novethic has broken this down too! According to their study, most of the growth came from fund conversions, inflows, and lastly (least significant) being performance & gains from the stock and bond markets.

|

| Source: Novethic |

Drilling down again..within these two, the growth in Retail investors was attributed to the growing awareness of SRI in the retail banking network. Secondly, the growth was attributed to popularity in employee savings plans.

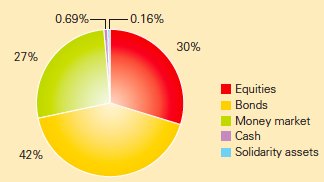

Breakdown of Investments:

A big surprise was the huge amount of money invested in non-equities. SRI is typically thought of as stocks/equities in the United States. However, given the nature of European investing (and the older demographic profile) it makes sense that most monies are invested in non-equities. These include Bonds and Money Market accounts. There were several money-market accounts that converted into SRI type funds.

|

| Source: Novethic |

Investing Approach:

ESG Screening, or what’s called Positive Screening on this website, was the most popular approach in French SRI. I consider this true socially responsible investing. So readers, please take note…Though Negative Screening was also utilized by several asset managers. This is far less popular in the States where asset managers are drawn towards ESG Screening/positive screening and Engagement/Shareholder Activism. In the US, shareholder activism amounted to $1.5 trillion, or about 50% of the total monies invested in SRI ($3.1 trillion). The Shareholder Activism style seems to fit well with the US’s “cowboy” culture.

French SRI versus U.S.

There are some key differences between how US asset managers invest in socially responsible companies, and those of our friends across the pond.

- the French are ardent believers of Positive Investing

- we, on the other hand, are focused on Shareholder Activism (see above)

- the French aren’t really convinced that SRI will bring extra-positive (“high Alpha”) returns to their portfolios, but are convinced it’s the right thing to do.

- on the other hand, Americans usually tout that such investing brings higher returns. In fact, there are now Hedge Funds –> link that employ quantitative SRI techniques to earn extra-returns on their investments. Some HF/asset managers don’t even care about it being the ethical thing to do, so long that returns are good.

- the French have huge amounts of Euros behind the SRI strategy

- in America, SRI, while in the trillions of $$, hasn’t yet reached mainstream, though it’s catching on quickly.

- French SRI, while grass-roots oriented, has also been motivated by the UN Principles for Responsible Investment, as well as the French government.

- American SRI is, of course, “laissez faire” – the American-way; and free from state/government intervention.

- the French aren’t too keen on “green investing“

- the opposite’s true on the streets of America, where people sometimes think that “green investing” is SRI. In fact, green investing has grown rapidly as its easily understood and can be marketed via exchange-traded (ETFs) and sector funds. (We will be publishing a piece/list on all of the ETFs available to both US and overseas investors.)

Then, where are the similarities?

Surprisingly, despite cultural differences, and several shades of gray in the definition of SRI, the United States and France have similar definitions of SRI. Please review our SRI trends articles for background information. Overall, we both strive to invest in companies that are doing good, either for their employees or their larger communities. We also agree on the various categories of SRI (e.g., Best in Class/Positive Screening) though each country tends to favor one category over another.

French SRI versus European ESG:

Thanks to Eurosif (in partnership with Novethic) 251 European investors were surveyed for the first time on their use of Environmental, Social and Governance (ESG) criteria into asset management. Eurosif (the European Sustainable Investment Forum) is a think tank whose mission is to develop Sustainability through European financial markets. Note that we are using SRI and ESG interchangeably, though ESG in this context/survey is a tad more broader, and less strict (the methodology is used more on a case-by-case basis than SRI which is more regimented).

Eurosif’s survey spanned nine countries during 2010 (totaling EUR 7.5trillion), with the largest being Denmark with huge SRI related assets of EUR 144bn. For comparison, the US market totals about $3.1 trillion (or about EUR 2.3 trillion). See our Update on SRI for additional information. Based on Eurosif’s survey, below are the key differences (and similarities):

- Both France and pan Europe overall have a strong understanding and definitions of what it means to invest for ESG. More than 90% of the asset owners surveyed believe that Positive/Best in Class Screening is SRI.

- France (along with Belgium) was the only country that didn’t associate ESG with investing in green companies/”clean tech.”

|

| Source: ESG Perceptions and Integration Practices, Eurosif, Novethic |

- About 84% of asset owners believe that there is no contradiction between integration of ESG criteria and their fiduciary responsibility. France, like most European countries has changed considerably in this area versus 5 years earlier, due to the release of the United Nations Principles for Responsible Investmentwebsite and due to government regulations.

- For comparison, in the US, we are still trying to figure out if SRI fits under ERISA’s Prudent Man Rule.

- I am not aware of any case law regarding SRI and (complimenting) the Prudent Man Rule.

- Click here for an interesting article on Fiduciary duties to pension funds and SRI.

- Most European asset owners surveyed believed that integrating ESG into their management contributes to long-term performance. The French don’t believe this, or invest for improved performance.

|

| Source: ESG Perceptions, Eurosif, Novethic |

- The French way of SRI was, as said earlier, investing in ESG positive screening, rather than Shareholder Engagement, which was more popular among Northern European investors.

- In terms of total Euros going to SRI, France was about in the middle of the pack compared to the other countries, led by Denmark. The Northern European countries dominated SRI assets, while southern countries such as Italy had smaller amounts of assets (EUR 13Bn)

Sources: Belsfi, Novethic, Social Investment Forum, Eurosif, Paris Europlace