SodaStream International Ltd. (SODA)

SodaStream is an Israeli company that makes and sells home beverage machines. These portable machines make flavored sodas out of ordinary tap water, or just seltzer/sparkling water. In order to make a flavored drink, SodaStream sells these products:

1. Soda Makers (Beverage Machines): to make the drinks

2. Carbonators (and CO2 refills): which make the drinks fizzy

3. Flavored Syrups such as root beer, colas

4. Bottles which the Soda Makers fill the soda into

For those unfamiliar with how the SodaStream system works, please take a few minutes to view this company video:

So what’s so special about SodaStream?

We believe there’s a time and a place for everything. Remember Apple’s Newton? Well, the time and place (United States) are now ripe for SodaStream. What we have here is a confluence of factos creating a whirlwind of demand for SODA. They include:

1. A self-aware and knowledgeable American consumer

2. The Greening of America

3. A weak economic recovery creating more “do-it-yourself” consumers

SODA’s products, for example, contain less sugar, its diet-versions don’t contain saccharin, and consumers can control the amount of flavorings that go into their drinks. Or like most people do, they can simply drink club soda/seltzer with no sugar at all. The company even sells an essence flavor that doesn’t contain sugar. In 10/2009, the company introduced a Sodamaker made with 85% recycled materials.

It is SodaStream’s job not just to manufacture soda machines but to educate the consumer that its products exist, show how they promote health & wellness, and help protect the environment (i.e, fewer disposable plastic bottles).

According to the U.S. Natural Marketing Institute, the “Green”Consumer Market is over $500Bn globally and over $200Bn in the U.S., and growing at a CAGR of 15%.

Overall assigned Rating:

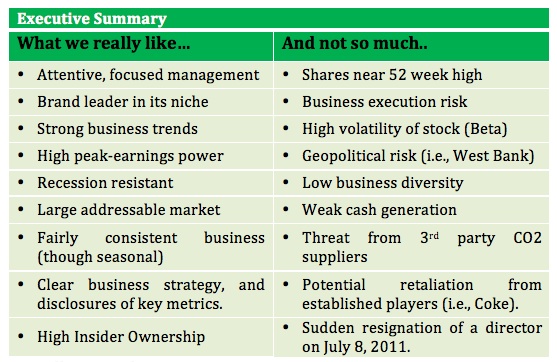

We believe SODA is a good SRI investment candidate. Our rating is “7” (out of a possible 10). This rating incorporates quantitative and qualitative factors, including the corporate, social and responsibility efforts.

The Executive Summary below summarizes key investment factors/risks. With the goal of maintaining objectivity, every investment is required to have a full list of Negatives, or if you will, “things we don’t like very much.”

Note: Earnings estimate is diluted, on 20mm shares outstanding, reflecting the 4/2011 secondary share offering. EPS converted at an exchange rate of $1.40/EURO.

Share Data for SODA reveals a company with moderate to high-priced shares, as measured by the Price to Earnings (P/E) ratio. The P/E ratio is high, but not huge on a PEG basis.

Note that the company is global, but based in Israel. So, it’s reporting currency is the Euro, but labor gets paid in Shekels. However, we report EPS data in dollars, as the shares are traded on NASDAQ.

Market Capitalization of <$2Bn categorize this as a Small-Cap investment, further increasing return potential, as well as risk. Our overall investment rating is 7, reflecting strong business trends, but higher-than-average share price volatility. Beta is 1.2x (co. went public in 11/10) however, we suspect it may actually be higher.

Our FY’2011 EPS estimate is based on 33% revenue growth and 73% net income growth, both higher than management guidance (+30%, +60% respectively).

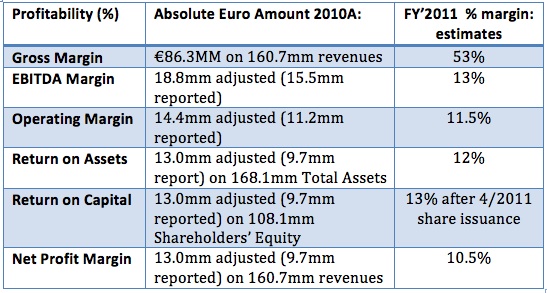

Revenues for Fiscal Year 12’10 were €161mm, up from €105mm the prior year. Over the last 3YR period, revenue and earnings have grown consistently with the exception of a “hiccup” in 2009 attributed to the Financial Crises. Data above is on an adjusted basis, which excludes a management fee (to former majority owner Fortissimo Capital) as well as non-cash compensation.

The Balance Sheet improved dramatically over the last year, as the company moved from an LBO to mainstream company. Shareholders’ Equity is high and much of the company’s assets are in working capital.

FY’10 Cash Flow was weak, after reporting two strong years. SodaStream reported positive Free Cash Flow in FY’08 and FY’09, but FY’10 FCF declined dramatically due to rising accounts receivables and inventories. We estimate A/R and Inv will be a $40-$50MM drag on yearly operating cash flow.

SodaStream’s profitability is expected to rise based on simple trend analysis. However, there are several short-term crosscurrents beneath the numbers readers should be aware of. Management fees to Fortissimo Capital affected FY’10 reported profits, and this will no longer continue.

Secondly, FY’11 operating margins will continue to be negatively affected by high Sales & Marketing Expenses, as management aggressively ramps-up business in the United States.

Thirdly, we expect the denominator to increase (on Capital) as the company issues common shares. There was a secondary common stock offering in April 2011, which will increase Equity over 25%, and decrease debt to negligible levels. Management is expecting 2011 net income to rise 60%, however this may not translate to EPS growth given the dilution effect.

Longer-term Profitability could rise sharply:

SodaStream’s business model is such that longer term (2013-2014) profitability could increase dramatically from 2009 levels even as revenue growth slows. By 2013, these factors may occur:

· Selling & Marketing expenses could decline as consumer awareness increases.

· The proportion of U.S. (i.e. “Americas”) revenue will increase dramatically. U.S. consumers love getting their “sugar fixes”, and thus, use more syrups than their European counterparts.

· A larger U.S. market will also benefit margins resulting from the distribution channel. This is because management has chosen to distribute directly in the U.S. Direct distribution has higher gross margins as the company typically sells its product at a discount to indirect distributors.

· The slice of Soda Makers’ share of the revenue pie will decline, as a larger proportion of sales will be attributed to high-margin Carbonators (i.e., CO2 bottles).

· Optimization of factory logistics, including the new factory being constructed will lower transportation costs.

· Operating Leverage should help increase earnings at a more rapid clip compared to revenue growth. This is because SodaStream has a fixed component to its cost structure as the company owns most of its factories. Further, half of its General & Admin expenses are fixed in nature.

· The dilution effect on EPS growth should decrease as the company becomes less dependent on external equity financing.

· Note that the above increase in expected profitability is expected despite our view that Carbonator margins will decline as new competitors enter the market.

Rather than reiterate the company’s statements, we highlight key data points and conference call comments:

· Performance was much better than expected by both analysts and management. So much so that SodaStream raised Revenue growth, from 25% to 30%. The company sharply raised earnings growth from 40% to 60%.

· SodaStream is experiencing rising raw materials costs especially for plastics (up 19%) and Sugar (up 14%) but so far has been able to pass through price increase to customers.

· Profits were boosted by strong consumables growth.

· Balance sheet debt declined to negligible levels.

· Operating cash flow remained negative, due to higher inventories

· The U.S. launch and ramp-up is performing better than expected.

· Company will launch into the Japanese market by 4Q’11.

· SodaStream will undergo a “big-box” retailer test this year

Overall liquidity is not high, but sufficient. SodaStream used a portion of its 4/11 secondary share offering to repay most of its debt. A small bank line, cash, and minimal debt maturities support liquidity. However, continued FCF deficit and higher (though transitory) capital expenditures for a new factory.

Most indicators of leverage are very low (minimal). Operating Leverage, while difficult to accurately measure precisely, appears high given the company’s ownership of fixed assets.

SodaStream’s FY’10 P/E ratio presents a rich valuation. FY’11’s is lower given the company ‘s rapid earnings growth. The PEG ratio of 1.4x would have been lower were it not for a 36% increase in diluted shares outstanding. In fact, we are forecasting a 70% increase in adjusted net income for FY’11. The EPS estimate is also subject to the ebb and flow of exchange rates, which we are basing on last year’s $1.4/EUR.

Other measures of valuation such as Price/Book Value, Price/Sales and Enterprise Value indicate SodaStream’s shares are fully valued. We also examined various Discount Models. Most indicated SodaStream’s shares were trading below calculated values (about 20% discount, on average).

However, we conducted a Discount Model utilizing FCF, which yielded a share price under $60. That calculated price is below the current trading price of SodaStream’s shares. Note that our model used more aggressive growth rates and a lower WACC than typically utilized, and we still could not achieve higher than $60.

This website utilizes CsrHub and Audit Integrity ratings given that they are a good standardizing and benchmarking tool for evaluating a corporation’s Corporate Social Responsibility efforts. Unfortunately, neither firm (including others such as RiskMetrics) was able to provide ESG ratings. This is attributed to the firm’s foreign (Israeli) incorporation and since its initial public offering was fairly recent (11/10).

However, what we can do is offer our opinion of the company’s accounting policies and disclosures. In both aspects, SodaStream appears above average. Disclosures are good, in fact, they seem better than what we’ve seen from most companies. This is likely attributed to its incorporation in Israel, which requires additional financial and operational disclosures. For example, several balance sheet items are footnoted, and detailed further in the company’s Annual Report.

In terms of the Environment, the company’s products are clearly beneficial compared to traditional methods of producing and distributing soda. For example, the SodaStream method of producing soda eliminates the need for disposable plastic bottles (and cans). Whilst true that both are recyclable, the fact is that only a small percentage actually gets recycled. Further, the carbon footprint and pollution created from transporting bottled soda is mostly eliminated using the SodaStream approach. We say “mostly” because it is true that its refillable CO2 containers do have to get transported to refilling stations. Management though, is aware of this and is establishing these stations logistically to reduce transportation.

SodaStream’s products also promote what’s commonly called Health & Wellness.” It does this by using sugar instead of high fructose corn syrup, offering less sugar in its flavors, using less caffeine, less sodium, and using better versions of sugar-substitutes (i.e., Splenda instead of saccharin). More recently, this author noticed SodaStream is now selling natural flavor essence, something very popular now in club soda.

How could SodaStream make its CSR Reporting better?

As seen from the above, SodaStream clearly has a healthy product and is environmentally friendly. However, we offer a short-list of recommendations if the company wants to be a truly Socially Responsible company. Essentially, the company should offer a CSR Report (perhaps integrated into its Annual Report initially). This report should include key metrics on:

· Environment: Data (yearly) on energy consumption and use of fossil fuels. Systematic programs that are used to reduce toxic emissions.

· Social: Employee benefits, diversity programs, work/life balance, etc. Metrics on factory safety.

· Suppliers: Monitoring of labor standards at suppliers

· Governments: Policy to address controversies in countries that have weak labor records, etc.

It is important that the CSR report not be a marketing piece about how great the company is. This is why it should have specific goals, and specific measurements to achieve them. It should also talk about “bad things” that happened to the company or its chief challenges. Speaking of which, the last bullet is of particular importance, if not urgent, concern to SodaStream given that its main factories are located in the West Bank (Mishor Adumim) Israel.

The West Bank was occupied by Israel during the Six-Day War in 1967 and the area is the subject of dispute between Israel and the Palestinian Authority. With the exception of East Jerusalem and the former Israeli Jordanian no man’s land, the West Bank was not annexed by Israel but remained under Israeli military control. Most of the residents are Arabs, although a large number of Israeli settlements have been built in the region since 1967. There has recently been negative publicity against companies with facilities in the West Bank. Several political groups have called for consumer boycotts of Israeli products (including SodaStream’s) originating from the West Bank.

SodaStream participates in the carbonated soda drink (“CSD”) and sparkling water industry. The industry is in the Maturity stage of its life cycle. The CSD industry is marked by low growth, high penetration, moderate competition and low revenue cyclicality. Industry revenues approximate $216Bn globally, according to Datamonitor. The sparkling water industry (i.e., seltzer, club soda) is $34Bn globally and far more popular in Europe than in the States. Both numbers exclude soda/sparkling water at restaurants. According to Euromonitor, the U.S. had the highest per capita consumption of 118 liters in 2010, approximating $39Bn in sales.

The CSD industry is experiencing flat growth, with most of it occurring in Emerging Markets. Revenue growth is fairly lackluster in Europe given the troubled economies of Greece, Spain, Portugal and Ireland. In the U.S., soft drink volumes had been growing in the low-single-digits in the ‘90s. However, volumes turned negative during the Financial Crises and have not recovered to previous levels. Name brand soda is also experiencing competition from white-label brands as well as niche drinks such as Energy and Sports Drinks (e.g. Hansen Natural).

YTD 2011 has shown incremental improvement, due to higher marketing spend. Companies have cited ongoing input cost pressures. SodaStream noted in its conference call (1Q’11) that Aluminum prices were up 9%, Plastic (+19%) and Sugar (+14%). Though, all participants have been able to recapture margins via higher pricing.

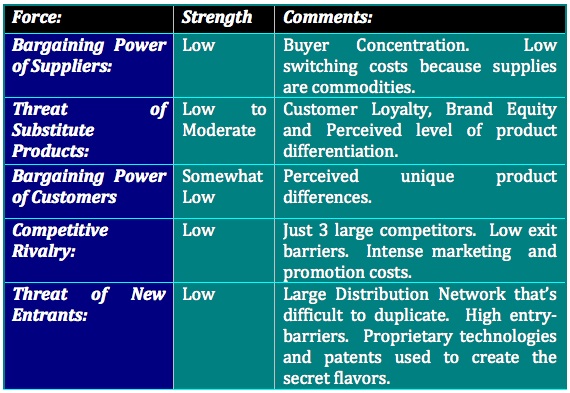

According to industry expert and Harvard professor Michael Porter, an industry can be analyzed using a Five-Forces Model. These forces determine how intense competition is within a particular industry. Industries with low intensity, are considered attractive, as they are profitable. Below we summarize these forces for the CSD industry.

As readers will soon notice, the soda industry structure is quite strong and oligopolistic. It is well protected and the threat of new entrants is low given high entry barriers and high promotional activity. Consequently, we expect there will be some retaliation and an answer to SodaStream’s market share advances.

|

| click to enlarge |

A peer group comparison indicates that SodaStream is much smaller than its brand-name competitors (i.e., Coco-Cola, Dr. Pepper Snapple, PepsiCo). Its (reported) profitability is also lower than most of its peers. However, SODA’s forward Price/Earnings ratio is higher than its peer group.

Management Summary:

SodaStream’s management appears highly focused, forthright, and attentive. In fact, they’re almost scientific about tactical market strategy. CEO Daniel Birnbaum is not only qualified in education and business experience, but he is a great “front man” for showing off the company’s products.

The existing management is fairly new, having been installed in conjunction with the acquisition and restructuring by Fortissimo Capital in March 2007. While new, senior managers have had experience working at Nike, Proctor & Gamble, Pillsbury, Kraft and McDonald’s.

SodaStream is now arming for battle at the home turf of the world’s most powerful soda companies. However, management also brings with it best practices from years of operating and entering new global markets (41 countries as of 1Q’11).

Management appears customer-centric, an important attribute in the Consumer Products industry. Note that several (four) executives have non-technical, social-type skills that may be giving it an edge above competitors. Mr. Tali Haim, for example, has a degree in Psychology and had been an organizational psychologist earlier in his career. After all, this business is really about consumer behavior !

Despite the 11/2010 IPO and 4/2011 secondary share offering, SodaStream insiders retain a significant ownership stake. We consider this very important in aligning executive interests with those of investors. As of 8/2011, insiders owned approximately 19% of SodaStream’s shares outstanding. In addition, Fortissimo Capital (the firm that LBOed SodaStream) continued to own at least 11% of the company’s shares.

Conclusion:

SodaStream’s a great company with somewhat richly-priced shares. Those interested in investing in the company are recommended to purchase on stock price retrenchments in the $50s area.

Disclosure: The author is long SODA. This article is neither a recommendation to buy or sell shares in SODA.